You Need to Sell Fuel Cell Stock Now, Before Everyone Else Does

In recent months, the surging interest in clean energy, electric vehicle, and battery electric stocks sent FuelCell Energy (NASDAQ:FCEL) to highs not seen since 2018. With no value or profitability, markets are turning a blind eye on fundamentals. FCEL stock is a perfect example.

FCEL stock has only positive momentum and decent promises for growth ahead to justify the nearly 15-fold return from 52-week lows.

Speculators should avoid getting caught up as short-sellers smartly build a nearly 16% short float against it.

Throughout the last few years, the fuel-cell powered company faced declining revenues and widening operating income losses.

A Closer Look at FCEL Stock

From 2015 to 2019, revenue dropped consistently as seen in the chart, right.

Notice the rising stock dilution in 2018-19. On Dec. 1, 2020, that common stock offering added another 34.5 million shares sold.

Although the $6.50 per share price is already up by more than three times at its price $20.94 peak last week, the gains could prove short-lived.

The company has an unfavorable debt-to-equity of 2.11 times and a long-term debt-to-equity of 1.92 times. Fundamental analysis is out of favor when the euphoria for clean fuel is driving the sector higher.

If that trend changes and markets grow cautious, FuelCell shares are set to plunge.

Bulls will owe the Biden pledge to invest billions in clean energy fueling the incredible returns in the sector. Bears may bet on FuelCell selling more shares to pay off its heavy debt and cover operating expenses again.

Capital Expenditures

The company needs to keep raising money to invest in the development and commercialization of its solid oxide platform. The company announced its plans in 2019, so it isn’t as if this is a new development.

“We have pursued development of a highly efficient and cost-effective solution using our patented solid oxide technology, with a particular design emphasis on a common cell stack design for this extensive range of applications,” CEO Chip Bottone said at the time.

Bulls are ultimately betting, again, on a bright future for FuelCell Energy. They need to differentiate between stock buying momentum and speculation and fundamentals.

Understandably, the firm is not profitable because of the capital cost requirements. Furthermore, cautious investors should watch for its progress in paying down its debt. In Nov. 2020, the company raised enough cash to pay down $87.35 million in debt.

A Weak Q3 for FuelCell

FuelCell posted revenue falling from $22.7 million last year to $18.7 million in the third quarter. Losses mounted, rising from a $1.1 million loss to a $10.8 million loss Y/Y.

Optimistic investors may point to its $1.33 billion backlog, but this still is a decline of $54 million Y/Y. A backlog does not necessarily translate to revenue.

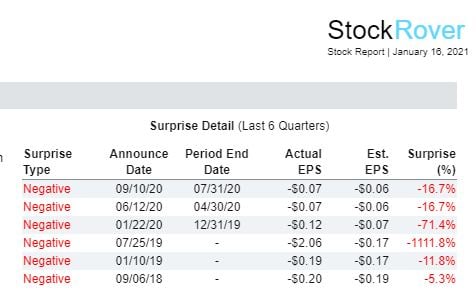

Investors should not be surprised when the company posts another miss. It did so in the last six quarters.

FuelCell faces the same risks. The clean energy stimulus will divide funds among many clean energy firms. FuelCell may get a small amount of it. This would undermine the bullish thesis and support the short-sellers’ bet against the stock.

According to simplywall.st, there is insufficient data to calculate what FCEL is worth. Analysts who rate the stock give it a “hold,” according to Tipranks. This is equivalent to a “sell” for investors who appreciate the hidden tone.

Dump FCEL Stock

FuelCell is a lottery ticket stock that paid off for investors who bought it a few years ago. After the run-up, those traders should consider locking in gains, but they should probably just sell the stock before everyone else does.

Disclosure: On the date of publication, Chris Lau did not have (either directly or indirectly) any positions in the securities mentioned in this article.

{kind=link}