Could C3.ai Stock Impress Wall Street With a 156% Return This Year?

Investing in C3.ai (NYSE:AI) stock could have been a straightforward proposition for 2022. Artificial intelligence (AI), big data analytics, and machine learning are arguably some of the most trending words in most corporate board meetings as business leaders craft strategies to futureproof their business models, improve efficiencies and create new competencies. Unfortunately, the AI stock price has fallen by 87% from its all-time highs printed in 2021. And Wall Street analysts seem divided on whether C3.ai’s shares should be on anyone’s buy-the-dip list right now.

C3.ai is a leader in the emerging enterprise AI space. It offers an AI application development suite, data analytics software, and sells a portfolio of industry-specific AI applications to a growing list of industries through software-as-a-service subscription contracts.

Shares are in free-fall, even as the company reports north of 40% year-over-year revenue growth rates.

Why Is AI Stock Falling as its Business Grows?

A recent short-seller report by Spruce Point Capital Management doesn’t help C3.ai stock price recovery right now. However, shares were on a downward trajectory well before the report. The house has not been in good shape for some time.

C3.ai’s business is evidently booming, at least on the revenue front, but the income statement is getting too ugly with each successive quarter. It ain’t clear whether the stock is a good investment candidate right now.

The company is a rapidly growing machine learning business, that fact isn’t arguable. A nice 41% year-over-year growth rate in quarterly revenue reported in December 2021 testifies to C3’s high growth status. Management was even overjoyed that the results exceeded market expectations. However, shares didn’t respond favorably.

Despite the fact that shares of tech companies that went public during the “best times” in 2020 were largely overvalued and needed a correction, AI stock investors have to shrug off the disappointing reality of increasingly bad earnings reports.

C3.ai’s operating costs are growing exponentially faster than revenue. Rising costs are destroying earnings and gobbling cash flows. C3.ai’s revenue is growing impressively, but operating income is taking a nosedive leading to the worst negative earnings margins ever seen since the company went public.

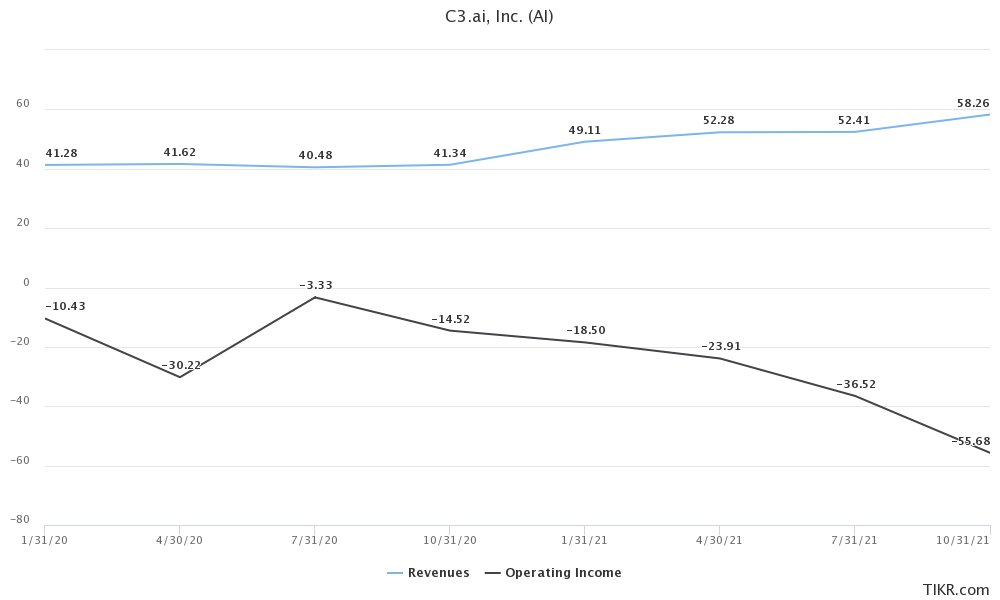

An excerpt of quarterly revenue and operating earnings for periods between December 2020 and October 2021 helps illustrate AI stock’s problem.

Ballooning Operating Costs Drag C3.ai Stock Down

Interpreting C3.ai Revenue and Operating Earnings Data

As can be seen in the chart above, any additional dollar in revenue added to the topline has increased the total operating loss by more than a dollar. Thus making growth seem somehow like an undesirable outcome right now.

For example, during the quarter which ended October 2020, the company booked $41.34 million in revenue and reported a $14.52 million loss from operations.

A year later, during the same quarter in 2021, C3.ai added $16.92 million more to the revenue line to report a 41% year-over-year growth to $58.3 million. However, quarterly operating losses increased by $41.16.

Therefore, an additional dollar in revenue increased operating losses by $2.43. That’s not an encouraging sign for the bulls. Actually, the data point strengthens bears’ resolve that C3.ai stock could still be overvalued.

Deeper losses help explain the high short-interest on AI stock which has been increasing since mid-year last year. Data from the StockRover fundamental data platform indicates short interest at 19.2%. A significant number of traders believe shares will continue to go down in the near term.

Wall Street Analysts Widely Divided on AI Stock Valuation

As things stand, analyst opinions on the company’s fair value widely diverge. This is especially evident in the insane range between the lowest and the highest analyst price targets on AI stock.

Those targets range from $35 a share up to $103 a share. An average price target of $59.13 indicates a potential 156% upside over the next 12 months. However, given the wide variance in analyst targets, investors should take the implied returns potential with a large grain of salt. AI stock price may never rise to anywhere near analyst price targets over the next 12 months.

Among other valuation considerations, widening losses and persistently negative cash flows fuel wide divergences in opinions by professionals following the company.

Moreover, there are growing concerns over the company’s revenue quality and sustainability. Specifically, a 32% growth in subscription revenue during the past quarter fell below analyst expectations. Subscription revenues are largely recurring. They offer better visibility into the company’s future earnings. This is unlike volatile professional services sales that may vanish in any random quarter.

A growth stock’s fair value is largely composed of the discounted value of its future growth opportunities. Consequently, poor visibility on the path to profitability and sustained cash flow generation on AI stock leads to higher divergence in expected values and levels of associated risk metrics used to discount any projected numbers.

It remains anyone’s guess as to when the business could start making profits for investors, let alone rack in positive cash flows.

Investor Takeaway

C3.ai is going through one of the riskiest growth phases of its corporate life cycle. There are no guarantees that massive hiring, aggressive marketing, and expansions in operating capacity will boost long-term business growth. Customer growth may fall behind cost increases, and the business may never scale to profitability.

That said, investors bullish on AI, big data analytics, and machine learning being the pillars of future corporate agility can buy C3’s stock right now as it yields to selling pressure and hold for the long term.

Investors shouldn’t take Wall Street’s price targets on AI stock too seriously though. Analysts have been adjusting their price targets on the company’s shares downwards for more than a year. They are likely to do so again in 2022 if shares trade lower or sideways for much longer.

On the date of publication, Brian Paradza did not have (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.

Brian Paradza is an investing enthusiast who was awarded the CFA Charter in 2019. A strong believer in fundamentals-based long-term investing, Brian learns from gurus like Warren Buffett but acknowledges human behavioral tendencies that drive short-term “madness”. You may find him inquisitive as he examines tech investing opportunities, cannabis, blockchains, and the new cryptocurrencies asset class.

{kind=link}